I opened my Help to Buy Isa six years ago after my step-dad told me I needed one as a first-time buyer hoping to get on the ladder.

I was 25 at the time and more pre-occupied with spending, instead of saving money – but now I’m taking home ownership seriously, and I’ve realised the account is useless and I’m stuck with it.

3

3

Experts call them “zombie” accounts because they’re slowly shuffling towards their expiry date, which is 2030, and many savers’ money is stuck in these accounts.

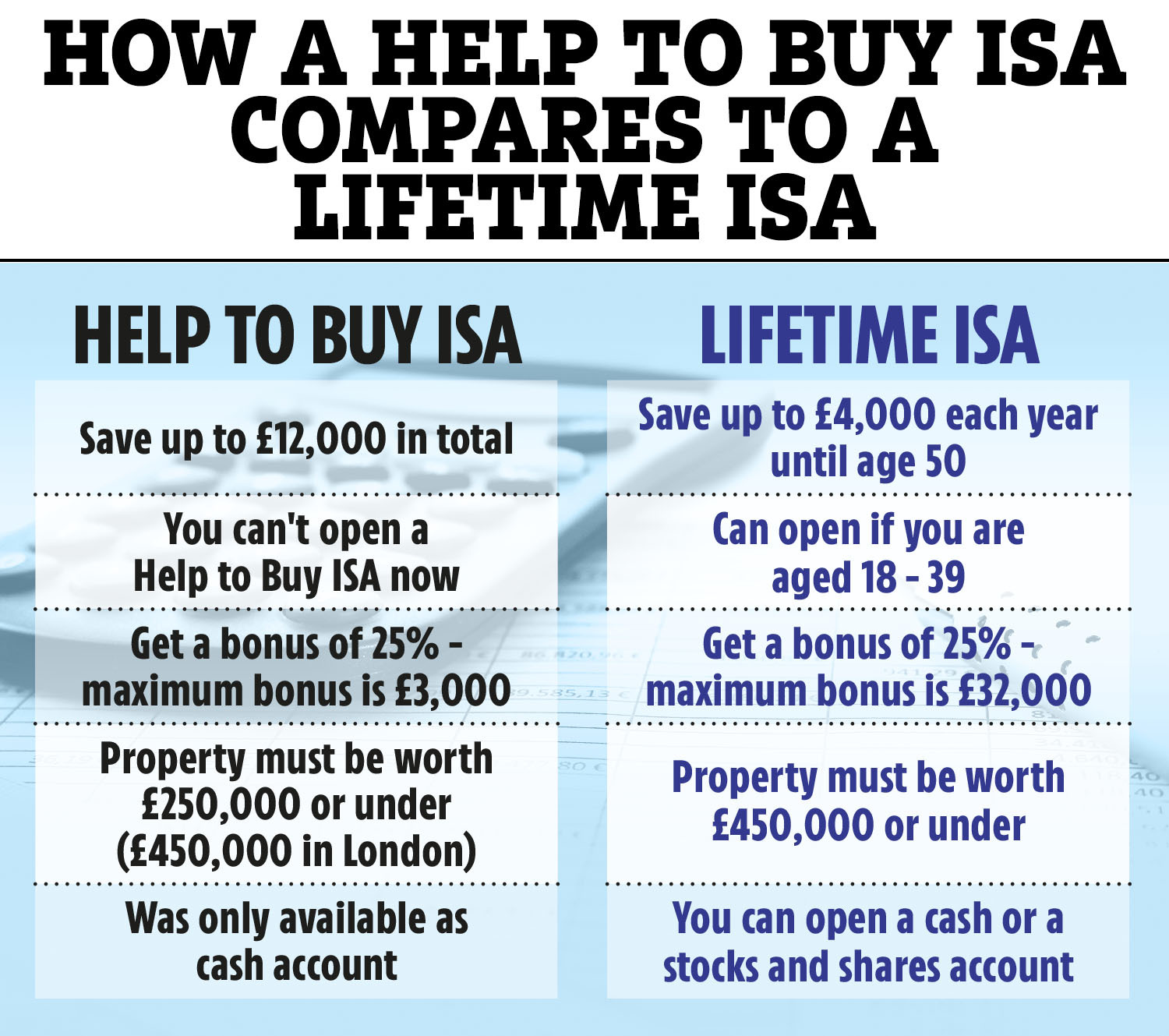

Help to Buy Isas were launched in 2015, and the big draw of opening an account was that you get free money from the government for your home.

The government gives you an extra 25% on top of what you have saved.

You can save up to £200 a month into these accounts, which means that for every £200 you save, the government adds £50, free, to your account.

Read more in money

For example, if I saved £12,000 (the maximum) I could get £3,000 extra in theory.

Sounds fantastic, but there is a drawback.

The Lifetime Isa came along in 2017 to replace the Help to Buy Isa.

Anyone aged between 18-39 can open one, and you can use it to save for a first home, or for your retirement.

Instead of a monthly savings limit, there’s a £4,000 a year savings limit on these accounts. Similarly, you get a 25% bonus from the government.

So in theory if I saved the maximum £4,000 a year from 18 to aged 50 (after this point, you can no longer save into the account), I would also get a whopping bonus of £32,000.

You can no longer open a Help to Buy Isa – applications closed in 2019, and you have until 2030 to get your bonus.

My issue is that I’m stuck with a Help to Buy Isa, when really, I want a Lifetime Isa – which is a bigger, better version of the Help to Buy Isa.

3

Pesky penalties

There are several issues I have with the Help to Buy Isa.

Me and my husband have been having serious conversations about whether to buy this year.

If we go ahead with this plan, I won’t be able to transfer my savings into a Lifetime Isa.

That’s because a Lifetime Isa needs to be open for at least 12 months to be eligible for a bonus.

Otherwise, I’ll have to pay a nasty 25% penalty on what I’ve saved in my account.

When savers are hit with this penalty, they end up losing the 25% government bonus, but also see 6.25% of their own hard earned cash taken as well.

Say you had saved £4,000 in a year, and earned a 25% bonus of £1,000. If you withdrew the total £5,000 in your account before 12 months has passed, you would pay a penalty of £1,250 – which means £250 of your own savings has been lost.

Many savers have been stung by this unfair penalty. Over £75million worth of charges were paid by savers in the 2023/24 tax year, according to figures from HMRC.

Another issue with the Help to Buy Isa is that the rules are way more restrictive.

To qualify for the 25% bonus, your property needs to be worth £250,000 or under (or £450,000 or under in London).

If you buy a property more than this amount, then you lose your bonus.

Me and my husband aren’t sure whether we want to stick in London or move to the country.

We need to stay close to the city for work reasons, so we would need to buy in the South East.

But with average house prices in this area at £380,428 according to the latest Land Registry figures, it’s likely that we would buy a property that busts through the £250,000 threshold.

The other annoying thing about a Help to Buy Isa is that you can only save a maximum of £12,000 into this account. That means the maximum bonus you can get is £3,000.

With a Lifetime Isa, there is no limit on how much you can save into the account – which means that you get more free money from the government with these accounts.

Also, the interest rates are often lower than what you can get on a Lifetime Isa.

The big downsides mean that many savers are stuck with these accounts.

Some two million people have a Help to Buy Isa with £5billion locked in them.

If you do want to transfer your savings out of a Help to Buy Isa and into a Lifetime Isa, you will have to drip feed the money into your new account.

You can save £4,000 a year into these accounts, so if you had £8,000 in a Help to Buy Isa, it would take two years to transfer out.

If you’re happy to make the transfer, you’ll need to open a Lifetime Isa first before you move your savings over.

Check websites like Which? to see which Lifetime Isas are the best.

I realise me and my husband are privileged to be in a position where we are thinking about buying.

But the issues with Help to Buy Isas just makes the whole process of getting on the ladder even trickier to achieve.

And if there’s one thing that would help boost the housing market – it’s having more first-time buyers being able to get on the ladder.

What help is out there for first-time buyers?

GETTING on the property ladder can feel like a daunting task but there are schemes out there to help first-time buyers have their own home.

Help to Buy Isa – It’s a tax-free savings account where for every £200 you save, the Government will add an extra £50. But there’s a maximum limit of £3,000 which is paid to your solicitor when you move. These accounts have now closed to new applicants but those who already hold one have until November 2029 to use it.

Help to Buy equity loan – The Government will lend you up to 20% of the home’s value – or 40% in London – after you’ve put down a 5% deposit. The loan is on top of a normal mortgage but it can only be used to buy a new build property.

Lifetime Isa – This is another Government scheme that gives anyone aged 18 to 39 the chance to save tax-free and get a bonus of up to £32,000 towards their first home. You can save up to £4,000 a year and the Government will add 25% on top.

Shared ownership – Co-owning with a housing association means you can buy a part of the property and pay rent on the remaining amount. You can buy anything from 25% to 75% of the property but you’re restricted to specific ones.

Mortgage guarantee scheme – The scheme opens to new 95% mortgages from April 19 2021. Applicants can buy their first home with a 5% deposit, it’s eligible for homes up to £600,000.